Consumer demands in the fashion market are growing more

complex and diverse by the day due to increased consumption

caused by higher incomes and rational consumption caused by

the economic recession. Other reasons include the demand for

individuality and personalized fashion, the expansion of lifeenriching

consumption such as leisure and cultural activities, the

increase in online purchases, the aging population and the shift

of core consumers.

With this polarization, a variety of fashion brands are expanding

into the global market, from high-end luxury brands like

Burberry and Louis Vuitton, to mid to low-end fast fashion

brands, such as Zara, H&M and UNIQLO, which have a strong

advantage in design, planning and distribution.

While global brands are competing in domestic and overseas

markets, the competition in global production is intensifying

through strengthened production and technological prowess.

This is a result of increased foreign investment into China and

Southeast Asian countries. Fashion products are also highly susceptible

to seasons and trends, thus making their life cycle short

while bringing in continuous demand. This creates sustainable

growth for the industry as consumers and preferences diversify,

so new products are developed to meet the changing needs of

customers.

The global fashion market has achieved an average annual

growth rate of 4.2 percent between 2009 and 2013, reaching

USD 1.54 trillion in 2013. The market is expected to grow at

approximately 4 percent annually until 2020.

By clothing type, the womenswear market is worth USD

638.1 billion, accounting for the largest share in the total market

at 41.5 percent. Menswear accounts for 27.6 percent and children's

clothing for 14 percent. Furthermore, products with newly

converged technology are growing at a rapid rate. The “smart”

trend is not only being developed in clothing which integrates IT

technology but also in the production and fashion distribution

process as well.

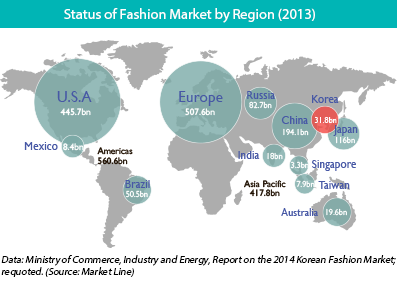

By region, the fashion market in America is worth USD 560.6

billion, accounting for 36.3 percent of the total

fashion market,

while Europe accounts for 33 percent with USD 507.6 billion,

and the Asia Pacific region for 27.2 percent with USD 417.8 billion. By country, the market size of the United States stands at

USD 445.7 billion (29 percent), China at USD 194.1 billion

(12.6 percent), Japan at USD 116 billion (7.6 percent), Russia at

USD 82.7 billion (5.4 percent) and South Korea at USD 31.8

billion (2.1 percent).

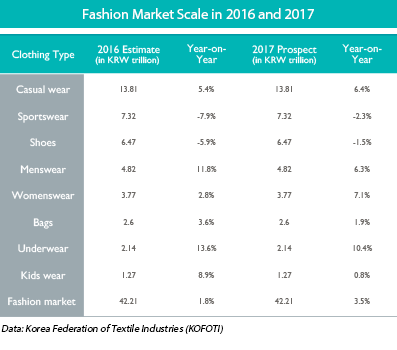

In Korea, the domestic fashion market continues to grow

despite uncertainties like sluggish domestic demand. This

growth is attributed to the rise of online and mobile shopping,

the diversification of new distribution channels and the diversification

of consumers. The focus of the fashion market is also

shifting from the sportswear market to the casual wear market,

while casual wear, menswear, womenswear and underwear are

showing consistent growth.

Production in the domestic fashion industry increased

between 2010 and 2014 because of the continued growth in

domestic demand and export volume. However, in the short

term, production volume has been on the decline since 2012

because of worsening domestic production conditions and

weakening demand for locally produced goods.

As a result, ever-changing local fashion trends, the continued

growth of fast fashion brands and increased exports of hallyu

(Korean Wave) content serve as positive factors for domestic

production. But production has somewhat dwindled as the

growing demand in the domestic market is involved more with

imported products than domestic ones.

Looking at the changes in the production structure of fashion

apparel, the share of shirts/workout clothes increased the most

with 28 percent of the total production in 2014. This is due to

the rise in the number of consumers who are interested in leisure

and health, as well as changes in lifestyle. In addition, the

boundary among the types of clothing such as casual style in

sportswear and outdoor wear has blurred.

While the export of fashion apparel increased by 4.4 percent

since 2010 because of the rising popularity and recognition of

Korean brands brought about by hallyu and improved product

competitiveness, clothing materials like textiles and fabrics,

showed a downward trend.

The increased export volume of such fashion apparel was

attributed to export growth in countries influenced by hallyu

such as Vietnam (24.2 percent), Taiwan (16.0 percent),

Indonesia (10.8 percent), Myanmar (9.34 percent) and China

(3.2 percent).

In particular, exports to Japan, which accounted for the largest

portion of fashion apparel in 2010, grew by 1.5 percent between

2010 and 2016, while exports to Vietnam surged by more than

20 percent during the same period.

Foreign direct investment (FDI) in the Korean fashion industry

has somewhat slowed down since 2013 but remains stable.

Unlike in the past when global fashion companies preferred

Japan or Hong Kong as their base for entering the Asian market,

they recently preferred to go straight to the Korean market for

Chinese and Korean consumers.

FDI, however, tends to be concentrated more on the distribution

of global fashion brands than on apparel manufacturing,

and it mainly includes joint ventures with global fast fashion

brands such as UNIQLO and Zara. Burberry and Gucci are

among the luxury brands that have directly entered the Korean

market to benefit from the sustained growth in the Korean fashion

industry and attract foreign tourists.

The most concentrated locations for the fashion industry in Korea include Seoul, Incheon and Gyeonggi-do, which

are leading

the trend and distribution sector and possess the largest consumer market. The knitting industry is concentrated in the northern

part of Gyeonggi-do and Jeollabuk-do.

The northern part of Gyeonggi-do is the world's top knitting

production area, and accounts for about 40 percent of the world

market for high-quality knitwear (golf wear, sportswear/leisure

wear, etc.), while accounting for about 90 percent of the domestic

knitting production. It is also the largest consumer of yarn,

consuming 60 percent of the locally produced yarn.

Jeollabuk-do is home to various producers, from the spinning

industry to the sewing and clothing manufacturing industry. It

also has a production structure mainly based on natural fibers

such as cotton yarn, knitting yarn and sewing, among others. In

terms of products, knitwear (which mainly includes underwear

and kids wear) is the mainstay of the textile industry in the

region.

In Busan, large-scale apparel companies, such as Parkland,

Indian, Colping and Greenjoy, operate a sewing factory

equipped with automation facilities. Facilities for OEMs are

located within a 50 km radius of Busan. The city's geographical

characteristics, its proximity to the sea, ports and an international

airport allow the fast introduction of global trends, giving

Busan strong logistics competitiveness and ease in promptly

responding to global demands. It has an abundant source of

technology personnel on standby and new skilled workforce

with its universities.

The global fashion apparel market volume in 2013 was estimated

to be worth USD 1.33 trillion, and it is expected to show

an annual growth rate of about 4 percent by 2020. As the market

boundaries between countries fall and the online-to-offline

(O2O) business strategies link online and off-line shopping, the

globalization and centralization of the supply chain from production

to distribution will accelerate.

The Korean fashion industry is also expected to grow steadily.

The country possesses world-class synthetic fiber materials

companies and infrastructure, and has the potential to utilize

convergence technologies such as information technology and

new technology.

As fashion apparel shifts to a small-quantity production structure,

the markets for fashion apparel are expected to be diversified

and converged with the growth of highly functional, designoriented

and smart clothes. Meanwhile, the increasing demand

for high performance and eco-friendly textiles and the diversification

of apparel consumption are expected to be a driving force

of the fashion market in the future.