fter Donald Trump’s surprising

upset win at the U.S. presidential

election, many countries—

if not the entire

world—are wondering what this victory

means for their own economy. Given that

Mr. Trump has quite the reputation for

being eccentric and somewhat bizarre,

many worry that he might carry out the

same eccentric and bizarre ideals in his

policies. But would he? The answer is no.

Running a country is not the same as running

a company. In a private company,

the CEO may be able to call all the shots,

but the president of the United States cannot.

First, the president must deal with the

Constitution. Second, he must persuade

Congress. Third, he still has to appease

more than half of U.S. citizens who have

not voted for him. Tens of thousands of

people have already rallied against him

all over the nation. Can he turn a blind

eye to them? Absolutely not. So among

all this uncertainty felt by the public, here

are some things we can be sure about.

First, under the Trump administration,

the Federal Open Market Committee

(FOMC) rate hike seems almost certain.

FOMC members have been deadlocked

for some time between the dovish and the

hawkish, rendering quick action almost

impossible. But this will change as Mr.

Trump is expected to fill two vacant seats

in the FOMC with the hawkish, making

them the majority. On top of that, the current

FOMC Chairwoman Janet Yellen

will be replaced by someone who will try

to pursue a rate hike. A higher rate will

benefit the people of the middle class as

they would be able to save substantially,

which in turns leads to more consumption

and consequently a more prosperous

banking industry. It will also make the

U.S. dollar stronger, giving U.S. citizens

greater purchasing power abroad, which

is good news to Korea.

Under the Trump administration, there

would also likely be huge federally

financed investments in infrastructure

across the nation. Bridges, airports, roads

and highways are expected to be renovated,

upgraded or newly built under the

new administration. These public works

will definitely raise the nation’s growth

rate. The federal budget deficit and government

bond issues may surge, but not

many will care as long as such decisions

boost US growth.

The Korean people have also been

closely following the election results, as

they are curious as to see what this means

for the Korean economy. In my opinion,

for Trump, pressuring either China or

Korea on trade and exchange rate issues

may be important but not as imminent as

the rate hike and infrastructure investment

projects in the U.S. This is because

trade talks with other countries require

lengthy and tedious negotiations before

both sides can come to an agreement.

Also, a booming U.S. economy accompanied

by a higher rate hike is one of the

best scenarios for Korea under the Trump

administration. First, Korea could expect

better export performance. As a major

part of Korea’s export performance is

affected by the growth of the U.S., a stimulation

of economic growth through

infrastructure investment would activate Korean and Chinese exports to the U.S.

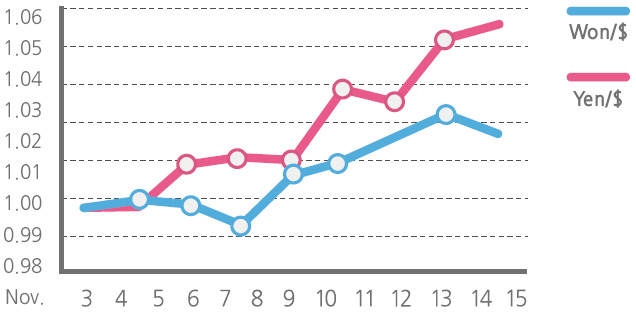

Furthermore, a higher rate in the U.S. will induce the depreciation of the won exchange rate, which is also conducive to higher export performance. Of course, some challenges might arise, especially as the Japanese yen depreciated faster than any other currency after the U.S. election. This may mean that Korea’s price competitiveness against Japan’s may slightly weaken. But despite some bumps in the changing of administrations in the U.S., the Korean economy won’t be heavily affected as long as exports continue to surge.