- Home

- Investment Opportunities

- Latest Information

- Industry Focus

Industry Focus

- Display

Date

2023.11.03

Status of the Display Industry

Display Industry: Expected to Continue Growing based on the Growing Markets for Premium Electronics and Convergence Products

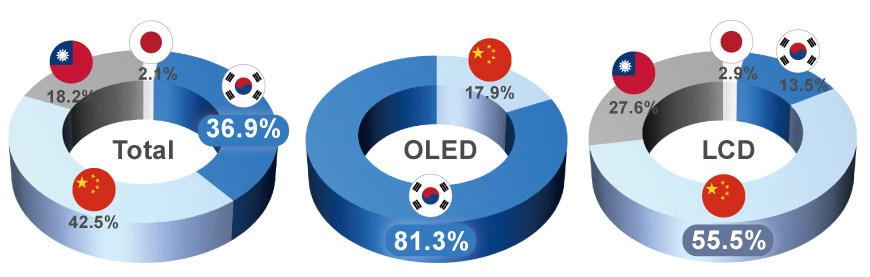

A display panel is an image displaying device (panel) that shows various information on a screen for people to see, and plays the role of the eye of the industry. Korea has maintained the world's top position in the display industry for 17 years since 2004, most notably in the field of OLED which is acknowledged as the next generation display. Korea leads the world with a global market share by maintaining the top place for 16 years (global market share of 81.3% as of 2022) after producing the first OLED in 2007.

Based on continuous R&D, Korea is leading the OLED technology by introducing the world's first rollable TV and foldable OLED. Korea's OLED production technology is three to five years ahead of its competitors, and while some small and medium-sized OLEDs are produced by competitors, Korea is the exclusive producer of large OLEDs.

In the 1990s, display panels were mainly produced by four countries in Northeast Asia (Korea, China, Japan, and Taiwan), starting with Japan's investment in LCDs. In recent years, however, Korea and China have emerged as major producers. China started leading the global market share from 2021 based on large-scale investment in LCDs, while Korea strategically reduced LCD production and focused on investing in OLEDs to expand production as panels are rapidly being adopted in major home appliances such as mobile phones, TVs, and other IT products.

Based on continuous R&D, Korea is leading the OLED technology by introducing the world's first rollable TV and foldable OLED. Korea's OLED production technology is three to five years ahead of its competitors, and while some small and medium-sized OLEDs are produced by competitors, Korea is the exclusive producer of large OLEDs.

In the 1990s, display panels were mainly produced by four countries in Northeast Asia (Korea, China, Japan, and Taiwan), starting with Japan's investment in LCDs. In recent years, however, Korea and China have emerged as major producers. China started leading the global market share from 2021 based on large-scale investment in LCDs, while Korea strategically reduced LCD production and focused on investing in OLEDs to expand production as panels are rapidly being adopted in major home appliances such as mobile phones, TVs, and other IT products.

World Display Market Share in 2022

* Source : KDIA, OMDIA(‘22)

Korea is proactively responding to new demand markets such as virtual reality, automotive, aircraft, architecture, medical, and interior by developing not only variable displays with no design restrictions such as foldable, rollable, and stretchable displays, but also transparent OLEDs and 3D displays such as holograms. After successfully mass-producing the world's first quantum dot (QD) display product in 2021, Korea is striving to develop next-generation technologies such as micro LEDs and micro displays for AR and VR while refining OLED technologies.orea plans to invest KRW 65 trillion by 2027 (2023-2027) to increase the production of QD-OLED TVs and expand OLED markets for mobile, IT, and automotive applications. Korea is expected to lead the trends of next-generation technology by producing OLEDs for IT products such as laptops and tablets as well as for mobile phones and TVs.

The Korean display industry centers on major panel producers (e.g., Samsung Display and LG Display) and manufacturers of materials, parts (822 companies) and equipment (473 companies) used in the panel manufacturing process. Manufacturing sites of Samsung Display (in Cheonan and Asan) and LG Display (Paju and Gumi) represent a display ecosystem densely concentrated with materials, parts and equipment makers. Notably, the Cheonan and Asan region housing Samsung Display was designated as a Specialized Industrial Complex for Strategic High-Tech Industries (in July 2023), laying the foundation for fostering the next-generation display market.

The Korean display industry centers on major panel producers (e.g., Samsung Display and LG Display) and manufacturers of materials, parts (822 companies) and equipment (473 companies) used in the panel manufacturing process. Manufacturing sites of Samsung Display (in Cheonan and Asan) and LG Display (Paju and Gumi) represent a display ecosystem densely concentrated with materials, parts and equipment makers. Notably, the Cheonan and Asan region housing Samsung Display was designated as a Specialized Industrial Complex for Strategic High-Tech Industries (in July 2023), laying the foundation for fostering the next-generation display market.

Market Outlook and Government Policies to Foster the Display Industry

As the Global Market is Being Reorganized with a Focus on OLEDs, the Government is Strengthening Support to Create a Super-Gap in OLED Technologies and Accelerate the Creation of New Markets

‘The global display market was valued at USD 118.1 billion in 2023 and is expected to grow to USD 135.6 billion in 2027. In particular, the overall market size continues to grow, driven by increased demand for premium electronics and the expansion of convergence display markets such as automotive and transparent display as more customers want free-form, ultra-high-resolution devices. Currently, the market is largely divided into LCDs (65%) and OLEDs (34%) displays, and other technologies such as Micro LED and OLEDoS make up the market. LCD is the largest market, but its growth is stagnating due to the wider OLED application to IT products such as monitors, while the market is gradually being reorganized with a focus on OLEDs due to their superior image quality, thickness, and form factor compared to LCDs. OLEDs are expected to lead the market growth by growing at an average annual rate of 3.7% by 2027.

The Korean display industry is driving innovation in the ICT market, but competitors are catching up fast. China continues to support OLEDs at the national level in addition to LCDs, while Taiwan and Japan are increasing their investment in next-generation micro LED technology to overcome their disadvantageous positions in the OLED sector.

In response to the challenges, the government announced the 'Display Industry Innovation Strategy' with a vision to secure super-gap technologies and regain the world's No. 1 position by 2027 through a joint public-private partnership.

The Korean display industry is driving innovation in the ICT market, but competitors are catching up fast. China continues to support OLEDs at the national level in addition to LCDs, while Taiwan and Japan are increasing their investment in next-generation micro LED technology to overcome their disadvantageous positions in the OLED sector.

In response to the challenges, the government announced the 'Display Industry Innovation Strategy' with a vision to secure super-gap technologies and regain the world's No. 1 position by 2027 through a joint public-private partnership.

Display Industry Innovation Strategy: Vision and Strategy

| Vision | Reclaiming the World's No. 1 Display by 2027 |

|---|---|

| Five Major Strategies | ❶ Fully support private investment ❷ Create 3 new markets ❸ Secure super-gap technologies ❹ Build a solid supply chain ❺ Develop human resources |

* Source: Display Industry Innovation Strategy to Reclaim the World’s No. 1 Position by 2027 (Press Release), MOTIE, May 18, 2023

The government plans to support private investment in all stages from R&D to production by providing tax benefits, policy financing and infrastructure and improving regulations so that the private sector can invest in a timely manner..

Five core technologies* of the display industry have been designated as national strategic technologies under the Act on Restriction on Special Cases Concerning Taxation (implemented in February) to provide companies investing in related facilities with corporate tax deductions of 15% for large and middle market enterprises and 25% for small and medium-sized enterprises and help ease the burden of investing. As companies producing related materials, part and equipment as well as display makers are eligible for the tax deductions, the law can widely benefit SMEs and middle market enterprises. In addition, the government facilitates investment by consulting with relevant ministries and local governments to ease regulations that companies find difficult to comply. As a result, inspections for new facilities handling hazardous chemicals and transportation procedures for large equipment were made more rational..

Moreover, the Korean government introduced a quota tariff system to strengthen industrial competitiveness and facilitate the supply of goods. The quota tariff is a flexible tariff system that can be applied temporarily by reducing the rate within the range of 40%p to the basic tariff rate for price stability and smooth supply. Since eligible items are selected through semiannual or annual demand surveys, companies planning to import a certain product needs to apply for the quota tariff in advance

Five core technologies* of the display industry have been designated as national strategic technologies under the Act on Restriction on Special Cases Concerning Taxation (implemented in February) to provide companies investing in related facilities with corporate tax deductions of 15% for large and middle market enterprises and 25% for small and medium-sized enterprises and help ease the burden of investing. As companies producing related materials, part and equipment as well as display makers are eligible for the tax deductions, the law can widely benefit SMEs and middle market enterprises. In addition, the government facilitates investment by consulting with relevant ministries and local governments to ease regulations that companies find difficult to comply. As a result, inspections for new facilities handling hazardous chemicals and transportation procedures for large equipment were made more rational..

Moreover, the Korean government introduced a quota tariff system to strengthen industrial competitiveness and facilitate the supply of goods. The quota tariff is a flexible tariff system that can be applied temporarily by reducing the rate within the range of 40%p to the basic tariff rate for price stability and smooth supply. Since eligible items are selected through semiannual or annual demand surveys, companies planning to import a certain product needs to apply for the quota tariff in advance

Foreign-Invested Companies Successfully Operating in Korea

The growth of Korean panel companies since 2000 has attracted many foreign companies to enter Korea especially in the fields of parts, materials and equipment. Most parts and materials companies produce glass and films in Korea while equipment companies include those producing in Korea and those installing, repairing and exchanging products. Corning Precision Materials was established in Korea as a joint venture between Samsung and Corning in 1995 and has been supplying glass, a key material for LCD production, to Korean companies. In April 2023, Corning announced an investment plan of USD 1.5 billion (approximately KRW 2 trillion) over five years to build an ultra-thin bendable glass manufacturing base in Asan, Chungnam Province, contributing to the establishment of a supply chain for the Korean display industry.

By Jo Eunsook ( (jes@kdia.org))

Head of Office, Industry Policy Team, Korea Display Industry Association

1) Global display market shares (%) : LCD (`22) 65% → (`27) 59% / OLED (`23) 34% → (`27) 37.4%

<The opinions expressed in this article are the author’s own and do not reflect the views of KOTRA.>