As the market leader of advanced technology,

Korea is using IoT to further boost its economic potential

In the wake of the mobile revolution, a new revolution called

hyperconnectivity is on the rise. And what’s emerging in the

middle of this transformation is ICBM—Internet of Things,

cloud computing, big data and mobile technology. This web of

connection among people, things and the online world increasingly

enables real-time collection, storage, analysis and utilization

of data.

The Internet of Things, or IoT, allows us to collect a wide

variety of data that traditional ICT couldn’t offer. Other than

being the groundwork for ICBM, IoT also provides analysis and

utilization of the data collected as well as real-time feedback,

thereby serving as a point of connection between the online and

offline world.

Therefore, IoT is not just a precursor to the full realization of

ICBM, but an essential element to the development and

improvement of any product or service.

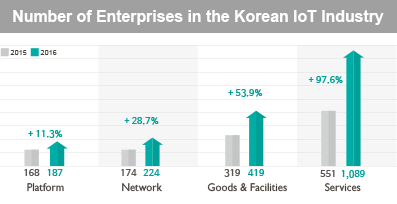

According to statistics based on Korean Standard Industry

Classification (KSIC), there are 1,991 IoT vendors based in

Korea as of 2016, an increase of 779 (or 64.3 percent) from

1,212 in 2015. The aggregated number of Korean enterprises

that offer IoT services stands at 1,089, up by 538 (or 97.6 percent)

from 551 in 2015.

There are also 374 and 125 companies newly registered under

‘Computer Programming, System Integration and Management Services’ and ‘Application Software

Development and Supply’,

respectively, resulting in new players to the IoT services market.

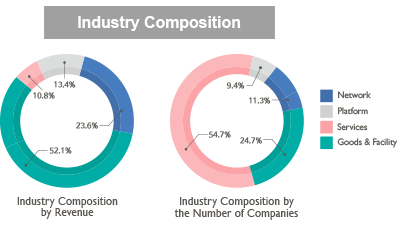

In terms of revenue, hardware solution sales stands at about

KRW 3 trillion (USD 2.7 billion), making up for around 52.1

percent of the total revenue generated in the area. Revenue from

network solutions stands at KRW 1.36 trillion (or 23.6 percent),

followed by KRW 771.57 billion (or 13.4 percent) from platform

solutions. While the 1,089 IoT service vendors account for

54.7 percent of total IoT firms, their share in the industry’s total

revenue is as low as 10.8 percent. And despite burgeoning entrepreneurship

in the area, the sum of revenue generated from IoT

services in 2016 went up by a mere 23.2 percent from the previous

year.

In terms of market structure, Korea’s IoT industry is relatively

dependent on goods and equipment compared to the global market.

According to the International Data Corporation (IDC)’s

latest ‘Worldwide Semiannual IoT Spending Guide (Jan 2017)’,

hardware represents the largest (30.6 percent) spending category,

but the structure is relatively balanced as services, software

and connectivity take up 27.5 percent, 25 percent and 16.9 percent,

respectively. This indicates the domestic industry’s

stronger dependence on goods and equipment.

The IDC also forecasted that modules and sensors that connect

end points to networks will dominate hardware purchases,

as hardware spending approaches USD 400 billion by 2020. Yet

hardware will be the slowest growing IoT technology group,

according to the market research firm.

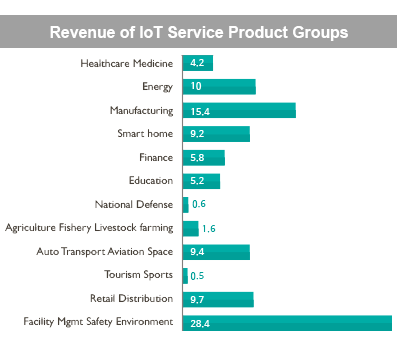

As for IoT services, majority of the revenue came from facility

management (entry and exit control, facility management,

attendance management services, off-site facility control and

monitoring, building crack monitoring, etc.), safety (locationbased

child tracking services, personal safety apps for women,

safety management for workers, toxic chemical monitoring at

industrial plants, etc.) and environment-related technology (air

and water quality monitoring and management, environmental

oversight, disaster control for fire and floods, etc.).

Revenue from manufacturing, or KRW 95.51 billion (USD

85.96 million) accounts for 15.4 percent. This is largely attributable

to the Korean government's policy effort to promote smart

factories, including the Banwol and Sihwa Industrial Complex

Smart Factory Cluster established last year.

Smart home and energy-related technology is showing the sharpest increase in revenue year-on-year. As mobile telecommunication operators entered the smart home market, the market's total revenue jumped by 54.4 percent, or KRW 20.06 billion (USD 18 million). Energy-related services also saw a 52.3 percent growth from 2015. In a report released in July 2016, the Hyundai Research Institute (HRI) suggested that smart home, smart cities and connected cars are the three most promising IoT-related products. The global market for smart homes is forecast to expand from USD 9.8 billion in 2015 to USD 43 billion in 2020; the number of devices connected to smart homes

via the IoT will shoot up to 44.15 million by 2020 from 7 million in 2015. IoT companies are also optimistic about the potential of IoT applications in smart home and energy. Many businesses thus expect smart home technology to be the fastest thriving market in the IoT sector.

Currently, business-to-business (B2B) transactions account

for more than 80 percent of the IoT services market in Korea,

while the share of business-to-consumer (B2C) transactions is a

mere 5.7 percent. The B2C market might be in need of market

stimulation as revenue generated from two major product

groups—healthcare/medicine and smart home—make up for 5.4

and 4 percent, respectively, of the aggregated total.

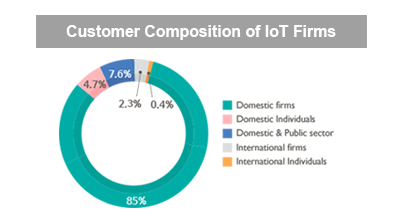

B2B’s dominance in the Korean IoT market is also visible in

the customer makeup. Domestic companies represent 85 percent

of all consumers, making them the biggest customer group for

IoT vendors. They are followed by domestic governments and

public institutions at 7.6 percent and domestic individual customers

at 4.7 percent.

Recognizing its potential as the next engine of economic growth, many countries are now turning to the IoT sector to solve national challenges, reform the public sector and boost private sector competitiveness. With its top-level ICT infrastructure, diverse and innovative startups and tech-friendly people, Korea has strong potential to become a leader in this field. Given the IoT’s potential to take the Korean economy to the next level, Korea should utilize the technology as a strategic tool to addressing national challenges such as economic growth, youth employment and other social issues.